Larry Smith, a known biotech analyst has an interesting analyst report on the recently released DCVax-D data and also touched about the reason why the share price has been so low, etc. Enjoy reading below (btw, he is the guy who coins the term wolfpack for the first time in regards to the concerted short attack on nwbo):

https://smithonstocks.com/northwest...ect-is-encouraging-nwbo-speculative-buy-0-43/

"

Expert Financial Analysis and Reporting

Northwest Biotherapeutics: Recent Data Update on Phase 1/2 Trial of DCVax Direct is Encouraging (NWBO, Speculative Buy, $0.43)

Posted

by Larry Smith

on Oct 9, 2016 • (

0)

Key Points:

- Data for DCVax Direct recently was updated for its phase 1/2 trial in 40 patients having 13 different types of inoperable solid tumors. A scientific paper showed that the top 12 patients (30%) experienced overall survival of 22 months or longer.

- This was an open label trial without a control group as is the case in almost all phase 1/2 trials. Results were compared to an algorithm (the Wheler system) developed by M.D. Anderson in 2012 that uses risk factors to predict survival of any individual patient based on certain risk factors. These can then be used to compare predicted life expectancy for each patient against the actual survival time. The average survival time predicted by Wheler for the top 12 patients is 12.3 months. With DCVax Direct treatment, they survived an average of 26.7 months and 8 are still alive. This suggest a remarkable doubling in average life expectancy by 14.4 months.

- This very long duration of response in about 30% of patients is impressive and compares very well with results that have been seen in trials of other immune therapies. For example, the hugely successful checkpoint modulators, Opdivo and Keytruda, as monotherapy have been shown to produce such long durations of response in about 15% to 20% of late stage non-small cell lung cancer patients and 25% to 30% of late stage melanoma patients,. These patients were generally earlier stage than those treated with DCVax Direct. This has electrified the cancer treating community.

- Another example is Kite’s highly touted CAR-T therapy (KTE-C19) which just reported interim phase 2 results in 51 r/r DLBCL patients. In those patients, 33% remained in complete response (CR) at three months. There can be no determination at this early date as to how these CRs may translate into length of survival. However, it is highly unlikely that all of the patients (33% of those treated) who achieved a complete response will survive two years. Kite is hailing these results as a medical breakthrough and states that they will support filing a BLA by year-end 2016.

- The Kite data and Northwest data deal with very different drugs in very different cancers; both use open label designs (no control group). I fully recognize the huge disparities in types of cancer patients treated, but the results have some similarity in that they treat very advanced cancer patients for whom there are no effective, remaining treatment options. To me at this point in time, results seem more promising for DCVax Direct or at the worst as promising and yet Kite has a $3 billion market capitalization and Northwest has $59 million. Go figure.

- This phase 1/2 data fully supports advancing DCVax-Direct into phase 2 trials. I had been expecting phase 2 trials with DCVax-Direct in two or three different inoperable solid tumors to begin in in early 2016. I discuss the reasons for the delay in this report.

- I note that Opdivo and Keytruda have been approved based on phase 2 data from open label trials in certain aggressive cancers that had no effective treatment options. Also, Kite is planning to file a BLA on interim phase 2 data. If NWBO achieves outcomes that suggest durable cancer responses in perhaps 15% to 20% of patients in one or more of its trials, DCVax Direct might also be approved based on phase 2 data.

- DCVax Direct has one major advantage over Opdivo, Keytruda and KTE-C19. It has a very mild side effect profile while those three drugs have serious grade 3 and 4 toxicities and KTE-C19 has been linked to deaths in the ZUMA-1 trial. The principal side effects of DCVax Direct are injection site reaction and grade and 1 and 2 fevers that can be treated with Tylenol. Remember that FDA decisions weigh risk to the patient as heavily as benefit in their regulatory decisions.

- I am by no means claiming that this data establishes that DCVax Direct is effective and will gain approval. However, I think that any objective observer would find the data encouraging and intriguing, especially when analyzed against the Wheler algorithm. It certainly warrants further investigation in phase 2 trials.

Other Investment Issues

The primary purpose of this report is to analyze the clinical trial data for DCVax Direct. However, I will first touch briefly on other key investment issues of the Company.

The initial announcement of the screening halt in the DCVax-L trial in August 2015 marked the beginning of a sharp fall in the stock. Initially it had only minimal impact, but a series of other events, most of which (in my mind) were wolfpack orchestrated led to a steady, rapid and disastrous decline in the stock.

Investors had initially expected a quick resolution to the screening halt, but disappointingly the Company has not yet offered an explanation for the screening halt nor has it provided any important updates on the trial other than several encouraging updates on the information arm relating to rapid progressors who were too sick to enroll in the trial, but received the exact same treatment as those in the trial. Based on company statements, I think that at least 300 (and possibly more) patients have been enrolled out of a planned 348. I think that results from this trial could be reported out by year end. See my

report “My Hypothesis as to Why the Company Has Been Silent on Its Clinical Trial Programs and Why DCVax-L Might Succeed in its Phase 3 Trial” for a more detailed analysis. This report also includes a more detailed discussion relating to my speculative buy rating on the stock.

Investors who have followed Northwest have watched an egregious short selling attack on the Company. I believe that the wolfpack (a group of hedge funds who work in coordination) have conspired to drive the stock price down. They have combined naked short selling with a propaganda campaign of immense breadth and sophistication, and have been successful in destroying the stock price. I won’t go through all of the large number of wolfpack tactics they have used but one that stands out was a report authored by anonymous hedge fund analysts who called themselves Phase V Research that was published on Seeking Alpha on October 29, 2015.

Numerous allegations were raised in the Phase V report, one of the more important of which was self-dealing involving Northwest, its management and its contract manufacturer Cognate. The Company’s primary outside stockholder Neil Woodford drew attention to the Phase Five report and called for an investigation of the Company thereby delivering an accurate shot to his foot. His action was a major factor in the stock price decline. We are awaiting the release of an independent committee which was formed in January 2016 to examine in part a long list of charges made by Phase V as well as a number of other blogs attacking the Company. The wolfpack appears also to have worked closely with law firms who launched lawsuits that coordinated with the Phase V report and other negative blogs by other authors sympathetic with the wolfpack.

Unrelated to the Phase V allegations, in April, 2016 NASDAQ cited NWBO for certain potential violations of stock issuance rules unique to NASDAQ. After ongoing discussions, in September, 2016 NWBO entered into a settlement agreement with Nasdaq that resulted in a change in status favorable to Northwest and its shareholders in regard to certain stock grants to Cognate, the Company’s contract manufacturer and affiliate.

One of the positive repercussions of this settlement is that it would appear to an outside observer that in the process of reaching this settlement, NASDAQ examined much of the same information about the NWBO/Cognate relationship as was covered in the Phase V report, and disagreed with Phase V conclusions. The NASDAQ settlement also eliminated some of the key factors upon which the original Phase V questionable claims were based, in turn potentially gutting the various wolfpack sponsored lawsuits based on the Phase V allegations. While it is not possible for an outsider to know what the independent committee (which still has not reported) is considering, it seems reasonable that they would take time to assess the impact of any NASDAQ resolution on both the pending lawsuits and the Phase V Report before acting and this may be the reason for the long delay in publishing its report.

I was expecting perhaps two or three phase 2 trials of DCVax Direct in two or three (inoperable) solid tumor types to begin in early 2016. As explained in this report, with favorable results these could be the basis for regulatory approval. I was also expecting a phase 2 trial of DCVax-L in combination with a checkpoint modulator (probably Opdivo) in recurrent glioblastoma to begin in the same time frame. Again success in the trial could be the basis for regulatory approval. Northwest has given no guidance on plans for these trials. The delays are almost certainly linked to the small management team of this small company nearly being overwhelmed in formulating responses to NASDAQ, the independent committee, the wolfpack lawsuits and the endless orchestrated articles and rumors.

Northwest is also in a financially stressed condition and this may have played some role in the delay in starting the phase 2 trials. Northwest has now fought through and answered many of the issues raised by the wolfpack. I think that from a logistical standpoint, these phase 2 trials could start at any time, but there remains uncertainty as to how much funding will be needed, when it will be raised and how much dilution this may cause to current NWBO shareholders.

Objectives of Phase 1/2 Trials; Putting the Results of the DCVax Direct Trial in Perspective?

The primary objectives of a phase 1 trial for a cancer drug are to: (1) evaluate the safety of the drug (or drug combination), (2) determine an optimal dose or dose range to produce a therapeutic effect, and (3) identify side effects at that dose range. Phase 1 trials typically enroll small numbers of patients with advanced cancer for which there are no effective treatments and in whom the disease is progressing (rapidly). Because of this, it is often difficult to gauge efficacy; also the mechanism of action of the drug may not directly address the cause of the cancer. Innumerable mutations occur in tumors so that effective treatment of one solid tumor might be totally ineffective in another. Even within a tumor type the mutations can be very different and respond differently or not at all to a drug.

Investigators look for signals of efficacy in phase 1 trials, but because of the reasons just cited, there may be no clear sign of activity even for a drug that goes on to phase 2 and 3 trials and is ultimately shown to be effective. The hope is that lessons learned in phase 1 can provide the information to identify patients most likely to benefit and the therapeutic dose or dose range. The phase 1/2 trial of DCVax Direct combines objectives for phase 1 and 2 in one trial. I think that this provided a clear path forward to designing phase 2 trials

Results from phase 2 trials in some cases are adequate to seek regulatory approval as we have seen in the case of the checkpoint modulators-Bristol-Myers Squibb’s Opdivo and Merck’s Keytruda. It is extremely interesting that Kite is guiding investors to expect approval of its CAR-T drug KTE-C19 on the basis of an interim look in a phase 2 trial, which is based on only 51 patients with r/r DLBCL. However, it is more often the case that the phase 2 trial is intended to further refine patient selection and dosage to design a phase 3 trial for regulatory approval.

I think it is possible that relatively small phase 2 trials of DCVax Direct in inoperable solid tumors, if successful, might be the basis for regulatory approval. As I will discuss in this note, we have seen very promising signals of activity and remarkable safety. I had thought that phase 2 trials in two or three different types of solid tumors could have been started in late 2015 or 2016. The short selling attack and resultant financial distress have delayed the start of these phase 2 trials.

Perspective on the Phase 1/2 Trial of DCVax Direct

The 40 patients enrolled in this trial were suffering from 13 different types of inoperable solid tumors. Let me explain why these are the sickest of the sick cancer patients. If possible, in treating any type of cancer the desired first step is to surgically remove (resect) as much of the tumor as feasible to rid the body of as many cancer cells as possible. In many, many cases the complete removal of the cancer is not possible due to its location or because it may have metastasized from the primary site to organs throughout the body. Let me give you the example of pancreatic cancer which is widely recognized as being among the most deadly of cancers.

The problem with pancreatic cancer is the inability to detect it at an early stage. The pancreas is deep within the abdominal cavity and unlike cancers such as breast, prostate or colon, there is no way to periodically check and to detect the cancer at an early stage and operate. By the time the cancer produces symptoms that lead to a diagnosis, it has often advanced to the stage 4 or the final metastatic stage and is inoperable. Also the anatomical position of the pancreas makes it difficult to operate without damaging surrounding vital organs.

The DCVax Direct trial was meaningfully different in that 40 patients with 13 different solid tumor types were treated. Generally, phase 2 trials focus on patients with a particular type of tumor or even a particular mutation of that tumor type. The heterogeneity was highly unusual in a trial of this size (40 patients). An intriguing aspect of DCVax-Direct is that its mechanism of action makes it potentially effective against all solid tumors and their mutated sub-types; this is a huge addressable market. DCVax-Direct is also unique in that it has a relatively benign side effect profile which is virtually unprecedented for a cancer drug. The principal side effects are injection site reaction and grade and 1 and 2 fevers that can be treated with Tylenol.

Interpreting Data from the Trial

The heterogeneity of the cancers treated makes it difficult to evaluate the results. Subjects had a median of 3 tumor sites within a range of 1 to 5 and had received an average of 3.1 prior treatment regimens. There was no control group and with so few patients per tumor type, how can investors judge if results are promising? The first time I looked at the results, my impression was they appeared impressive as most key opinion leaders feel that in inoperative solid tumors, most patients die within six months to a year. However, without a control group this is speculative.

Again let me turn to inoperable late stage pancreatic cancer to illustrate issues of patients treated in the trial. Stage 4 inoperable pancreatic cancer is treated with chemotherapy or perhaps just palliative care which involves pain relief and supportive nursing. The primary and most widely used chemotherapy agents are gemcitabine (Gemzar) and erlotinib (Erbitux). Other drugs like oxaliplatin, irinotecan, leucovorin, and fluorouracil (5-FU) are sometimes used. These chemotherapy regimens have low objective response rates and produce little increase in median overall survival.

The pivotal trial of gemcitabine that led to its approval compared gemcitabine to 5-FU (essentially a palliative treatment) in stage 4 pancreatic cancer. The one year survival rate for gemcitabine was 18% versus 2% for 5-FU. A subsequent trial compared gemcitabine alone versus gemcitabine and erlotinib. The median overall survival for gemcitabine plus erlotinib was 6.2 months versus 6.9 months for gemcitabine alone. The one year survival rate for gemcitabine was 17% (in line with the earlier study) and was 23% for patients receiving erlotinib combined with gemcitabine. There have been numerous other combination regimens that have been tried but none have produced meaningful increases in median overall survival with acceptable side effects. I think that we can generally conclude that median overall survival is six months and about 20% of patients live for one year for this cancer type.

There are other aspects beside the heterogeneity of patient selection that make the results of this trial difficult to interpret. Some are listed below:

- Patients were scheduled to receive six injections over 32 weeks, but most patients actually received only 3 injections over 2 weeks, with some receiving a 4th injection at 8 weeks.

- There was no retreatment.

- Patients were only injected at one tumor site. It seems to me that injecting at multiple tumor sites, as is planned for phase 2, would result in a better effect.

- Three different cell dose levels were studied so that the number of cells injected might have been sub-optimal in some patients.

- Patients had varying risk factors such as performance status, and had undergone (and failed) varying prior treatment regimens with some patients having failed as many as 5 or 6 prior regimens.

- All patients were late stage 3 or 4 status patients. Results in earlier stage cancers might have produced better outcomes.

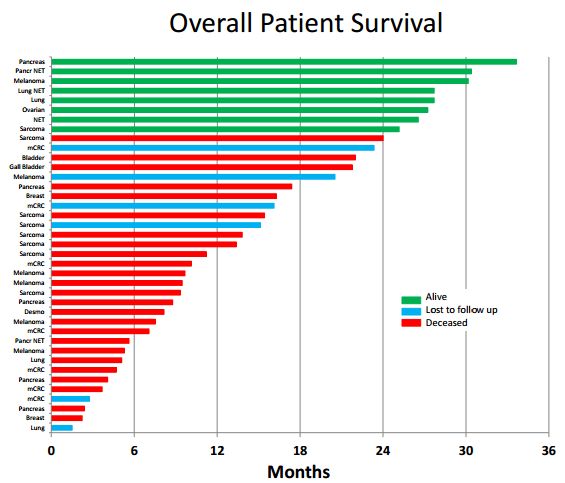

The following waterfall plot shows the outcomes in the 40 patients. Remember that in inoperable pancreatic that six months median overall survival is probably a reasonable expectation and that perhaps 20% of patients will be alive after one year. The best result in the trial was a pancreatic cancer patient who has survived 33 months. You can read about that patient in my

report National Geographic Special Features DCVax Direct Treatment of Stage 4 Pancreatic Cancer Patient.

From the above table it appears that 12 out of 40 patients (30%) had a dramatic result (and without retreatment). We have seen this type and level of response in other immune therapies like the checkpoint modulators Opdivo and Keytruda. As monotherapies, about 15% to 20% of non-small cell lung cancer and 25% to 30% of melanoma patients achieve long durations of response (long survival tails). The response increases with combinations, but toxicity does also.

More recently the highly touted CAR-T therapy from Kite (KTE-C19) reported that in 51 r/r DLBCL patients treated that 33% remained in response at three months meaning that 67% had progressed. It is likely that the 33% result will drop over time (perhaps significantly). Kite is hailing these results as a medical breakthrough and promising that they will file a BLA based on these results. Investors seem to have bought in on this as reflected in its $3 billion market capitalization.

Viewed against this backdrop, does the 30% of DCVax Direct patients remaining alive at about two years mean anything? I think so, but the hedge funds who are heavily short the stock put a negative spin on these results. They stress that there is no control data to compare against (which is almost always the case in phase 1 trials), and point out the small number of patients treated. They maintain that the long term survival just reflects outliers who are expected in any trial. While they are obviously putting the most negative spin possible on the results, an objective observer cannot categorically conclude or demonstrate that they are wrong.

An Interesting Way of Comparing Reported to Expected Results

In the latest paper on DCVax-Direct, a very interesting and more revealing way of interpreting the data was used. This was based on research done at the prestigious cancer center M.D, Anderson (who incidentally performed the DCVax-Direct phase 1/2 trial). In 2012, Wheler et al. provided a basis for determining life expectancies for an individual cancer patient. The Wheler system was based on examining a database of 1,181 patients who were treated at M.D. Anderson. NWBO applied the already established Wheler system to determine individual life expectancies for individual DCVax-Direct patients.

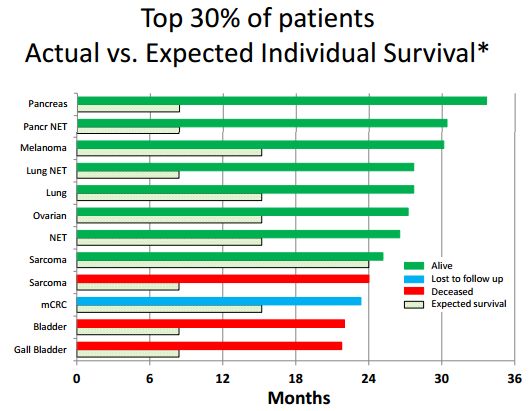

Most clinical trials compare aggregated or median results in a group of treated patients versus a control group. This is difficult or not feasible in small trials. Hence, it can be argued that individual patient assessments with the Wheler method provide more specific information than median survival measures. This methodology can be especially useful in exploratory early stage trials such as the DCVax Direct trial. Using the Wheler method, individual life expectancies were determined for the top 30% of the patients in the DCVax-Direct phase 1 trial, who have lived ≥22 months to date.

Here is how the Wheler system works. It assesses five risk factors for each patient: (1) serum albumin, (2) serum LDH, (3) number of metastases, (4) GI tumor, and (5) ECOG performance status. Scores for a particular DCVax Direct patient were determined using the Wheler system, and an individual life expectancy for that patient was determined. The Wheler system was based on scores in a data base of 1,181 diverse patients. Under the Wheler system, the expected median survival is 24.0, 15.2, 8.4, 6.2, and 4.1 months for patients with 1, 2, 3, 4 or 5 of the above risk factors, respectively. For example, a patient with five risk factors would be predicted to live 4.1 months.

Using the Wheler algorithm as a gauge, these risk factors were assessed and reported on for the 12 patients achieving the best response in the DCVax Direct trial. The individual life expectancies predicted for these DCVax-Direct patients are plotted in the following waterfall plot as the shaded horizontal bars, while the actual survival is plotted as solid horizontal bars. The average expected survival for these 12 patients based on the Wheler algorithm was 12.3 months and the average actual survival time was 26.7 months, for a highly impressive difference of 14.4 months.

F-Stein Weighs In on the Trial

F-Stein Weighs In on the Trial

In his latest of what is now 30 negative blogs on Northwest, Adam F-stein decided to give all of us a lesson in interpreting clinical trial data in a blog called “Biotech School: How to Spot Hidden Danger Signs in Clinical Trial Data.” He modestly informs us that “Using Northwest Bio as an example, I'm going to teach you how to read clinical trial data to find red flags and bad stuff biotechs don't want you to know. These "results" -- I struggle to even call them that -- amount to meaningless hand-waving.”

It is striking how venomous F-stein is in his attacks on the Company without even a faint attempt at objectivity. In this article he takes his usual tack of creating a strawman argument and then destroying it. He claims that the NWBO presentation compared an individual patient’s survival with the median survival for a whole group of patients or a whole category of cancer, and that is like comparing apples and oranges. In fact, NWBO compared individual patient life expectancies based on the Wheler system with individual patient actual survival to date – i.e., apples to apples. It was F-stein who tried to compare individual DCVax Direct patient survival times to median survival times for patients with diverse types of cancer, in his effort to discredit the data. In actual fact, the only one comparing apples to oranges was F-Stein.

It is a waste of time refuting what is clearly another biased F-stein article with limited (if any) meaningful insights. However, I would point out that F-Stein seems to have not understood or given no credence (probably both) to the Wheler algorithm which is so useful in putting the DCVax-Direct results in perspective. Or perhaps, he holds M.D. Anderson research in contempt as he does me and anyone who thinks that the DCVax vaccines are something more than grapefruit juice. Because his article mirrors the negative spin of the shorts, it may be of interest to compare

his article to mine.

I am by no means claiming that this data establishes that DCVax Direct is effective and will gain approval. However, I think that any objective observer would find the data encouraging and intriguing, especially when analyzed against the Wheler algorithm. I am certain that if F-stein reads my article that he will respond with a personal attack against me that Clinton or Trump could not aspire to. I have become inured to his personal attacks."