巴菲

知名会员

- 注册

- 2004-01-18

- 消息

- 290

- 荣誉分数

- 8

- 声望点数

- 128

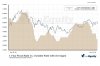

从历史的角度来看,原来近几年OTTAWA房价的总增长量还是算低的哦!下面是OREB的统计数据...

YEAR AVG SALES PRICE % CHANGE

1956 " $ 13,351 " 0.2

1957 " $ 14,230 " 6.6

1958 " $ 15,564 " 9.3

1959 " $ 16,038 " 3.1

1960 " $ 16,791 " 4.7

1961 " $ 16,070 " -4.3

1962 " $ 15,952 " -0.7

1963 " $ 16,549 " 3.7

1964 " $ 16,563 " 0.1

1965 "$17,056" 3

1966 "$18,004" 5.6

1967 "$19,476" 8.2

1968 "$23,329" 19.8

1969 "$25,652" 10

1970 "$26,532" 3.4

1971 "$27,808" 4.8

1972 "$30,576" 10

1973 "$38,305" 25.3

1974 "$46,661" 21.8

1975 "$49,633" 6.4

1976 "$54,623" 10.1

1977 "$57,032" 4.4

1978 "$59,134" 3.7

1979 "$61,896" 4.7

1980 "$62,748" 1.4

1981 "$64,896" 3.4

1982 "$71,080" 9.5

1983 "$86,245" 21.3

1984 "$102,084" 18.4

1985 "$107,306" 5.1

1986 "$111,643" 4

1987 "$119,612" 7.1

1988 "$128,434" 7.4

1989 "$137,455" 7

1990 "$141,438" 2.9

1991 "$143,361" 1.4

1992 "$143,868" 0.4

1993 "$148,129" 3

1994 "$147,543" -0.4

1995 "$143,193" -2.9

1996 "$140,534" -1.9

1997 "$143,873" 2.4

1998 "$143,953" 0.1

1999 "$149,650" 4

2000 "$159,511" 6.6

2001 "$175,971" 10.3

2002 "$200,711" 14.1

2003 "$218,692" 9

2004 "$235,678" 7.8

2005 "$244,531" 3.8

2006 "$255,889" 4.7

2007 "$272,618" 6.4

2008 "$290,366" 6.6

YEAR AVG SALES PRICE % CHANGE

1956 " $ 13,351 " 0.2

1957 " $ 14,230 " 6.6

1958 " $ 15,564 " 9.3

1959 " $ 16,038 " 3.1

1960 " $ 16,791 " 4.7

1961 " $ 16,070 " -4.3

1962 " $ 15,952 " -0.7

1963 " $ 16,549 " 3.7

1964 " $ 16,563 " 0.1

1965 "$17,056" 3

1966 "$18,004" 5.6

1967 "$19,476" 8.2

1968 "$23,329" 19.8

1969 "$25,652" 10

1970 "$26,532" 3.4

1971 "$27,808" 4.8

1972 "$30,576" 10

1973 "$38,305" 25.3

1974 "$46,661" 21.8

1975 "$49,633" 6.4

1976 "$54,623" 10.1

1977 "$57,032" 4.4

1978 "$59,134" 3.7

1979 "$61,896" 4.7

1980 "$62,748" 1.4

1981 "$64,896" 3.4

1982 "$71,080" 9.5

1983 "$86,245" 21.3

1984 "$102,084" 18.4

1985 "$107,306" 5.1

1986 "$111,643" 4

1987 "$119,612" 7.1

1988 "$128,434" 7.4

1989 "$137,455" 7

1990 "$141,438" 2.9

1991 "$143,361" 1.4

1992 "$143,868" 0.4

1993 "$148,129" 3

1994 "$147,543" -0.4

1995 "$143,193" -2.9

1996 "$140,534" -1.9

1997 "$143,873" 2.4

1998 "$143,953" 0.1

1999 "$149,650" 4

2000 "$159,511" 6.6

2001 "$175,971" 10.3

2002 "$200,711" 14.1

2003 "$218,692" 9

2004 "$235,678" 7.8

2005 "$244,531" 3.8

2006 "$255,889" 4.7

2007 "$272,618" 6.4

2008 "$290,366" 6.6

)

)